|

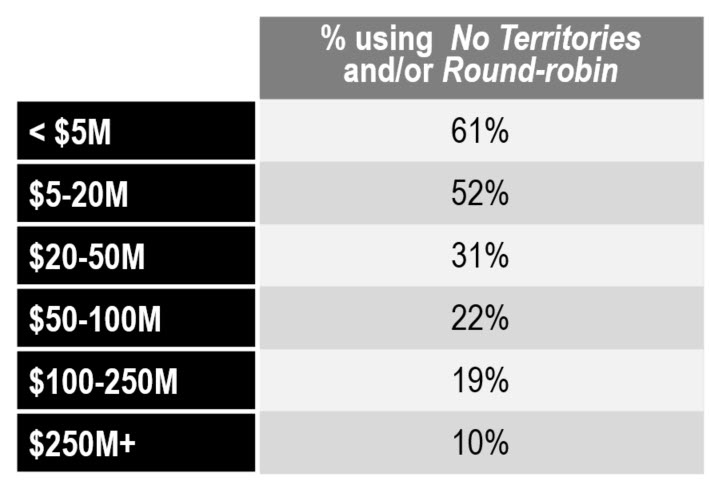

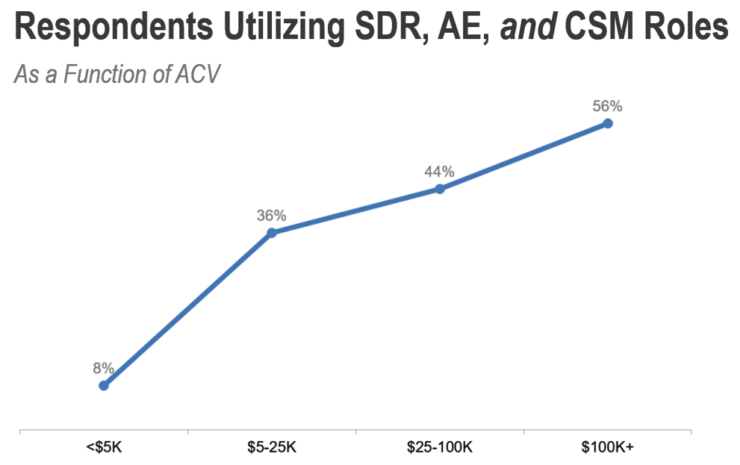

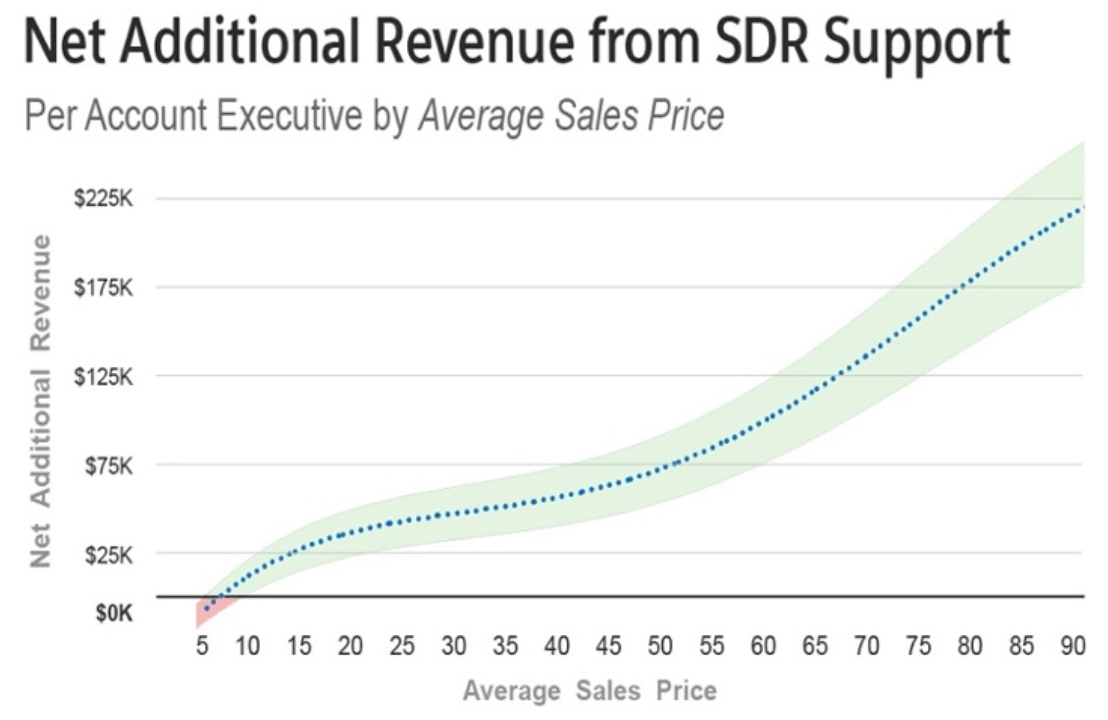

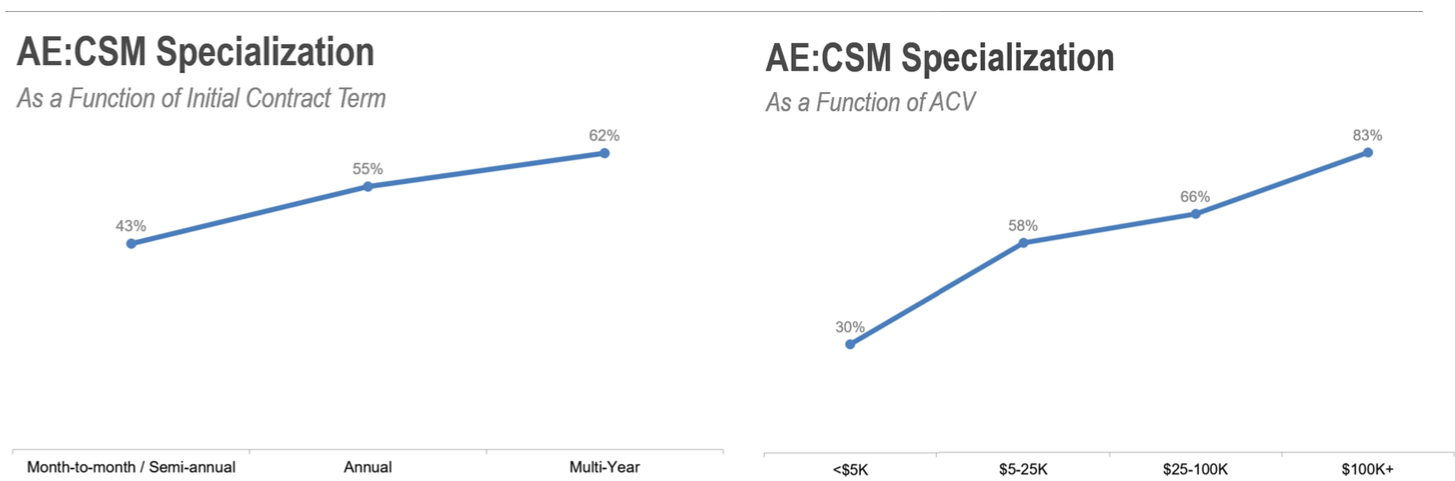

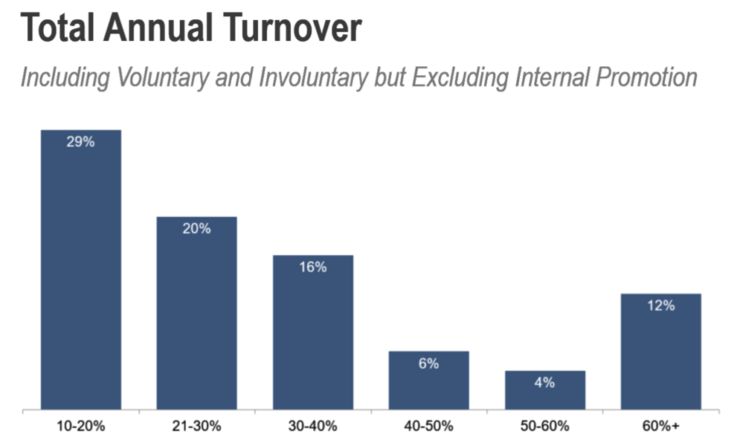

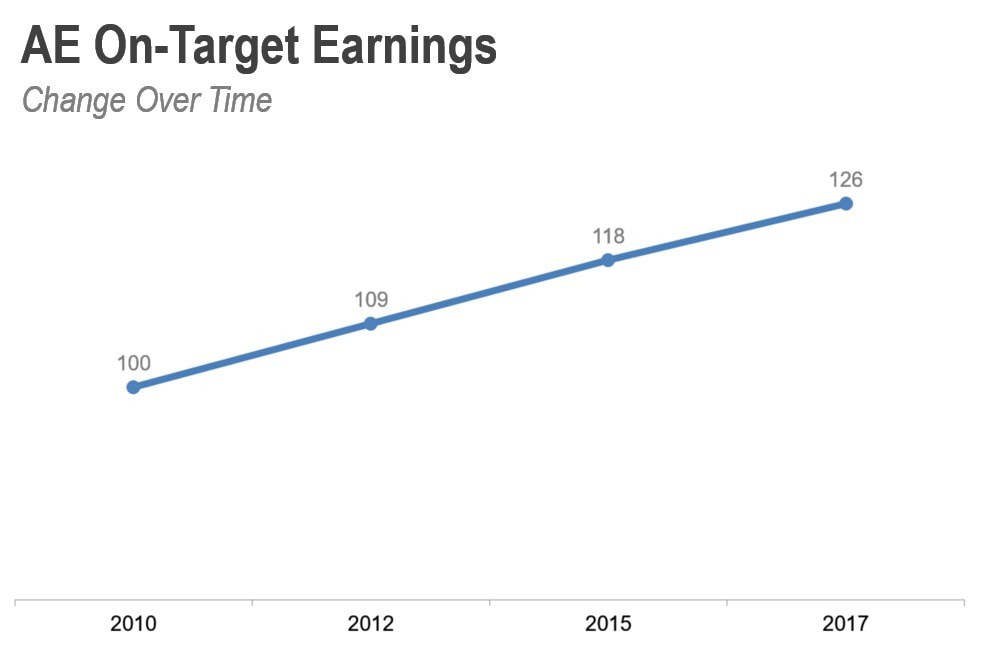

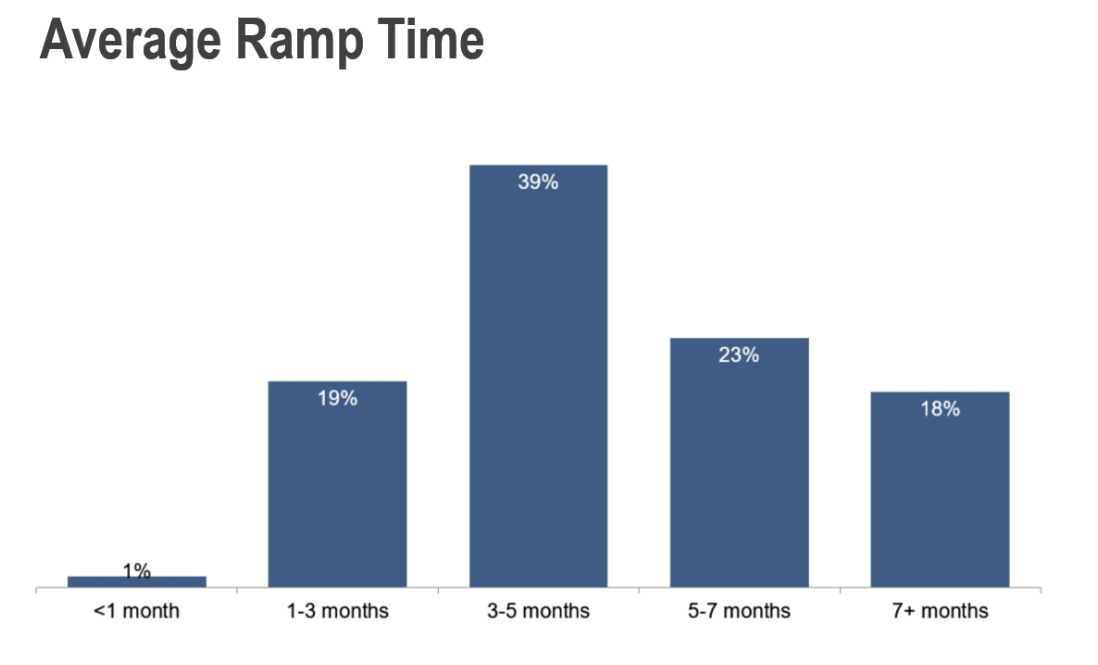

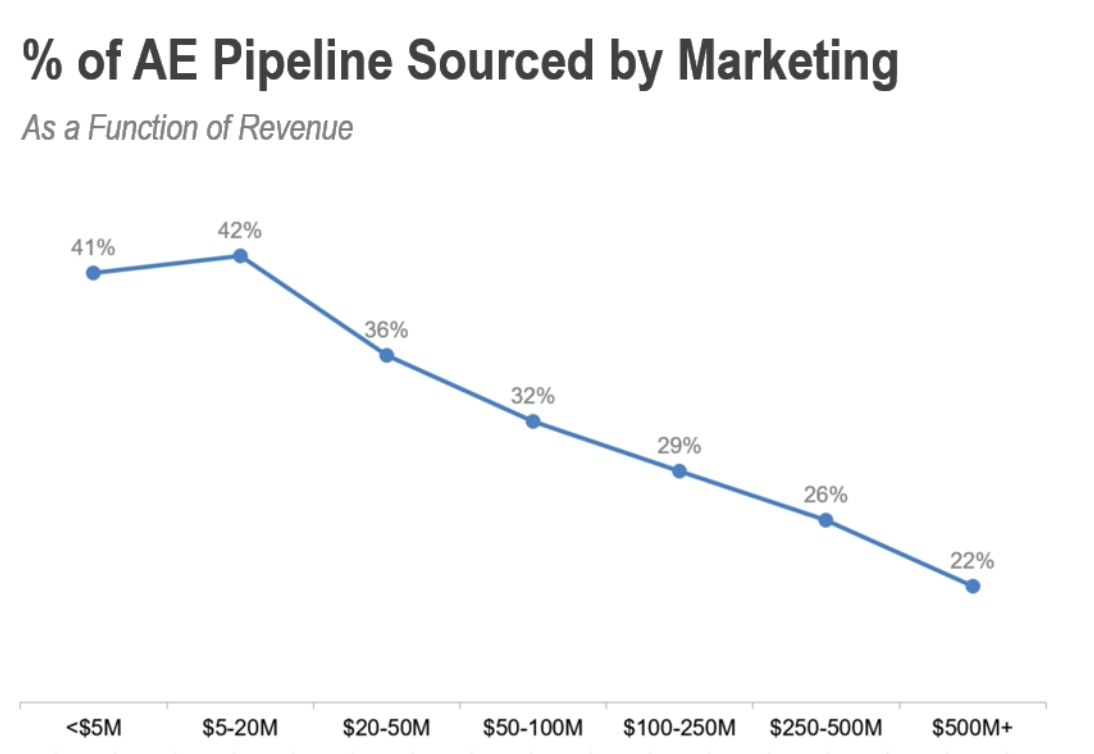

David Skok of Matrix Partners and the team from the Bridge Group are back again this year for their Account Executive report for 2017 — this is now the tenth year of the report where they track how metrics and compensation for this sales based role has shifted over time. SaaS, and other recurring revenue businesses face growth challenges due to the revenue for their services being fed in over an extended period of time, so this report offers specific analysis and recommendations based on high quality data to help inform the way SaaS companies build out their sales strategy and consider changes to their sales organization to optimize these revenues. Here are some top key takeaways and trends (kept as brief as possible): TERRITORIES STILL REIGN Building geographic based territories continues to be the leading approach, especially for earlier stage companies ($0-$20m in annualized revenues). Beyond those revenues, territory based approaches drop off significantly (obvious trend here is keep things simple until you can’t at ScaleUp). Interesting side point is that about 50% of the companies surveyed have sales reps working in different geographic regions. A few factors at play that explain this but mainly it’s the adding of offices via acquisition and highly competitive markets in certain regions for staff.  THE SALES DEVELOPMENT REPS (SDR’s), ACCOUNT EXECUTIVES (AE) and CUSTOMER SUCESS (CSM) COMBO OF ROLES REMAINS STRONG. The higher the Annual Contract Value (ACV) a company has, the more important these distinct and specialized roles are. For companies under $5m ARR these positions are generally not split out as specialized roles.  SDR SUPPORT 66% of the account executives surveyed are supported by SDR teams and this did not seem to vary based on company revenues, but SDR’s add more value (via revenue) at higher ACV’s — see chart below. SDR’s generate positive returns only on ACVs greater than $4k. For non revenue KPI’s, those AE’s supported by SDR’s see an average of 9.8 meetings per month. Outbound sales development (via SDR teams) generates roughly 1/4 of the total pipeline of an AE. Keep in mind that outbound prospecting is expensive so companies that have overall lower ACV’s, an outbound sales development channel may be difficult to justify.  CSM SEGMENTATION 50% of companies split new business revenues and renewal revenues into specialized roles for management (AE’s and CSM’s). Only companies with smaller revenues ( less than $5m ARR) keep these roles combined. Also noteworthy is that companies with month-to-month or seminary annualized contract terms are less likely to split out these roles. With companies that do split out roles, account are transferred from AE’s to CSM’s after an average of 3.6 months from close.  ACCOUNT EXECUTIVE TENURE and ATTRITION Average rep tenure sits at 2.4 years, (with an average prior experience of 2.6 years) but there seems to be a strong correlation to increased tenure and increased ACV. Average AE turnover sits at 30% (this is both voluntary and involuntary attrition).  ACCOUNT EXECUTIVE COMPENSATION & QUOTA Average on target earnings (OTE) now sits at $126K with average base salaries at $62K. Mix is generally in the 40% to 60% range of base to OTE. Average annual quota was found to be $770K in ACV and on average, quota was found to be 5.3X OTE — which remains stable across ACV and company annualized revenues.  AE’s are expected to ramp up at about the 4.5 month mark (which is up 20% from 2015)  67% of AE’s achieve quota — this metric has remained pretty consistent over many years. 2/3 of reps meeting quota is a good metric to gauge. There is much more data on quota, OTE and commission within the report, I suggest taking a deeper dive on compensation as it is varied based on ACV and plan type. MARKETING, MARKETING, MARKETING On average, 36% of an AE group’s pipeline is sourced by marketing.This includes inbound SDR support, but excludes outbound sales development efforts. The earlier stage the company is though, the more dependent they are on marketing as a source of revenue

1 Comment

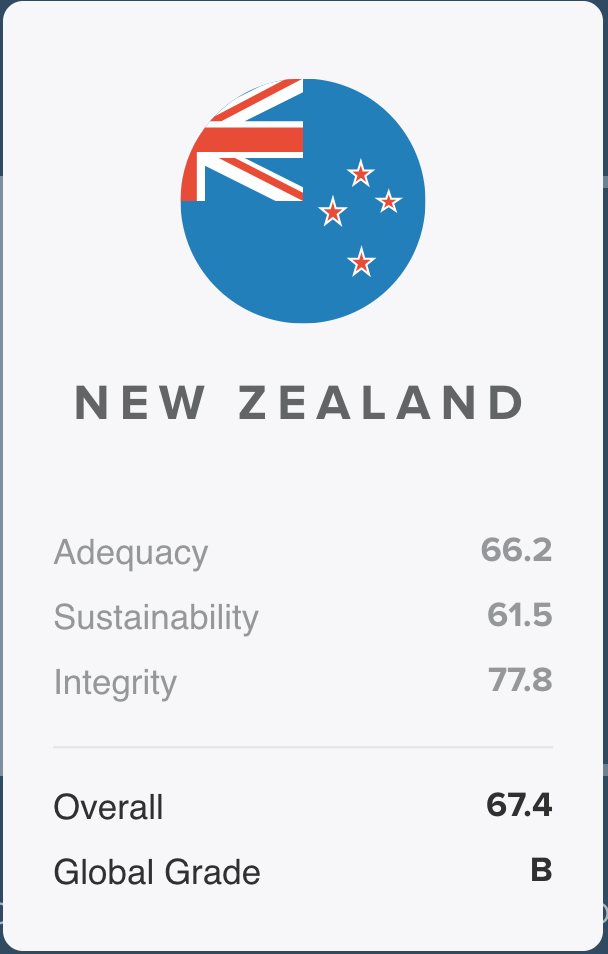

This year, for the first time, the Melbourne Mercer Global Pension Index, which benchmarks retirement income systems around the world, included New Zealand in the report - issuing an overall "B" rating. That’s actually an OK performance (no country received an “A” rating) and New Zealand performed well when it came to the integrity of the system and government. But it was let down by the adequacy and sustainability assessment section, getting a combined rating of 67.4 (out of a possible 100), placing New Zealand in 9th place overall. This means there is plenty of room for improvement and the report recognized the following areas of focus that could increase future scores:

There are currently about 2.8 million people signed up to Kiwisaver in New Zealand who have, collectively, invested $40 billion into the various schemes. However there are still 500,000 working-age people that are not registered, with many who are registered in the scheme not contributing anything to it, and many more are set to default contribution and investment settings, meaning that their future savings potential is far from optimized. Recently the New Zealand Financial Market Authority (FMA) discussed it’s disappointed with the level of personalised financial advice, specifically for KiwiSaver members, referencing a 2015 report that found just one in a thousand people getting tailored advice when joining or switching a Kiwisaver scheme. The FMA also recently refreshed it’s strategic outlook and identified rapid technological change as an emerging theme that it needed to be prepared for and last year the government also announced proposals to reform legislation governing financial advisers in an effort to streamline the different types of advisers and advice If you are a Kiwisaver member you are entitled to know what's going on with your funds, and get access to the right kind of financial advice to decide what type of fund is best for your personal savings or retirement goals. These default Kiwisaver accounts were never intended to be permanent and the timing is now right to make your next move. A lot happened in Tech this week. Like a lot. And the week isn’t even over. Most of this was due to some very significant conferences happening in San Francisco; primarily Facebook’s F8 conference and Amazon’s AWS Summit. Immersive, AI and Voice experiences were the key themes and these are the trends for the future of the internet. Which is why it makes this weeks activity and announcements pretty important. Below are the highlights: AMAZON — Voice is the new Internet Voice assistants are changing the way we interact with the internet and Amazon Lex, which is the artificial intelligence (AI) technology behind Amazon’s Alexa voice assistant, is now available to all developers starting this week. Opening up this platform means that developers can build more voice and chat enabled apps powered by Amazon’s Alexa (including New Zealand’s own ARDA) and because it is integration focused, they can also be published within existing chat platforms such as Facebook’s Messenger or Slack. What’s important here is that AI is only as good as the data it leverages over time, so opening up Alexa in this way will give Amazon a big jump on competitors. Amazing side note: Amazon Web Services (AWS), which a lot of Alexa based services will integrate with and run on, now also accounts for 1/3 of all of Amazons job openings (Amazon currently have a whopping 16,800 vacancies!!)  FACEBOOK — AR and Chat is going prime time Facebook is a company with many interests but this week they made a massive statement within the Augmented Reality (AR) space (as well as to continue to rip off SnapChat) by announcing an AR platform that will provide developers the tools to create products that recognize physical surroundings. Some of the new features unveiled by Facebook include a Camera Effects platform, not very dissimilar to SnapChats, which includes an AR Studio and Frame Studio that third-party developers can contribute to. The latest iteration of Messenger Platform was also launched and seems to have an increased emphasis on businesses and commerce. For example Mastercard announced partnerships with three retailers that enable chatbot purchasing inside the Messenger app. This marks an interesting move towards what the Credit Card company calls “conversational commerce,” Oh! And as part of Facebooks progression into AR and VR (and ripping off more of Snapchat), they also launched some camera hardware with two 360-degree cameras. The main difference here is that Facebook doesn’t plan on selling the cameras themselves. Instead, Facebook plans to license the x24 and x6 designs to a “select group of commercial partners.”  Facebook also owns Oculus so it’s interest in immersive video will not be primarily focused on the social networking side of the business, but immersive video viewing has been in a feature in the Social Network feed for a while. SNAPCHAT After several months of teasing a product, Snapchat chose this week (likely due to the F8 conference) to release “World Lenses”, which is their newest AR product set. Both Facebook and Snapchat are now competing not just as Social Media competitors but as AR platforms. But the use case metrics can’t be ignored here — FB outcompetes Snapchat big time and the “Stories” feature in Instagram, which is a total rip off of Snapchat Stories, now has more Daily Active Users (DAU) than Snapchats.  APPLE — in the Enterprise Not to be outdone in the announcements space, Apple made its iWork productivity suite (the Apple version of Microsoft Office) and iLife applications (GargeBand and iMovie) free to all iOS and macOS users on Tuesday. This is an effort by Apple to keep iOS and Mac users within the Apple ecosystem and to streamline access to productivity apps for enterprise users — which Apple is making serious headways into. MICROSOFT — buhbye passwords! We all know that passwords are the worst and Microsoft feels your pain — but only if you are a Microsoft user. This week they introduced a new way for users to sign into Microsoft accounts that removes the need to remember your latest password, you just need to remember your phone, which we all know that none of us leave home without. More on how that works here. GOOGLE — Earth (not) VR Google Earth had a complete reboot this week that was 2 years in the making and is ready with interactive guided tours. Interestingly it is not quite VR ready yet and I’m not quite sure what to make of that except that I’m positive it is on the Google Earth road map Multi voice recognition is now available to Google Home. Which means homes can now register multiple users with Google home products, and recognizes them by voice. This likely makes Google Assistant, the engine behind Google Voice, the main competitor to Alexa (sorry Siri!) GO-PRO — VR CameraGoPro is struggling to remain relevant after a rough 12 months. Today the company took the wraps off a new spherical camera called Fusion which is a device designed for creating fully immersive content (at 5.2k) as well as non-VR video and still photos. This now pits Go-Pro firmly against Snapchat and Facebooks Camera efforts.  |